5 Different Types of General Ledger Accounts

A general ledger account contains all the financial records of the company. It is also called the “principal book, which lays the foundation of the bookkeeping and accounting for the business. It is necessary for the preparation of financial statements—the income statement, balance sheet, and cash flow statement.

A general ledger also helps file the taxes. For example, if you pay taxes on behalf of an employee, you keep track of how much you paid in a given fiscal year to determine your tax liability.

Types of General Ledger Account

The general ledger is divided into sub-ledgers or different general ledger account types in which different financial transactions are recorded. The GL can be mainly categorized into five Types of General Ledger Accounts:

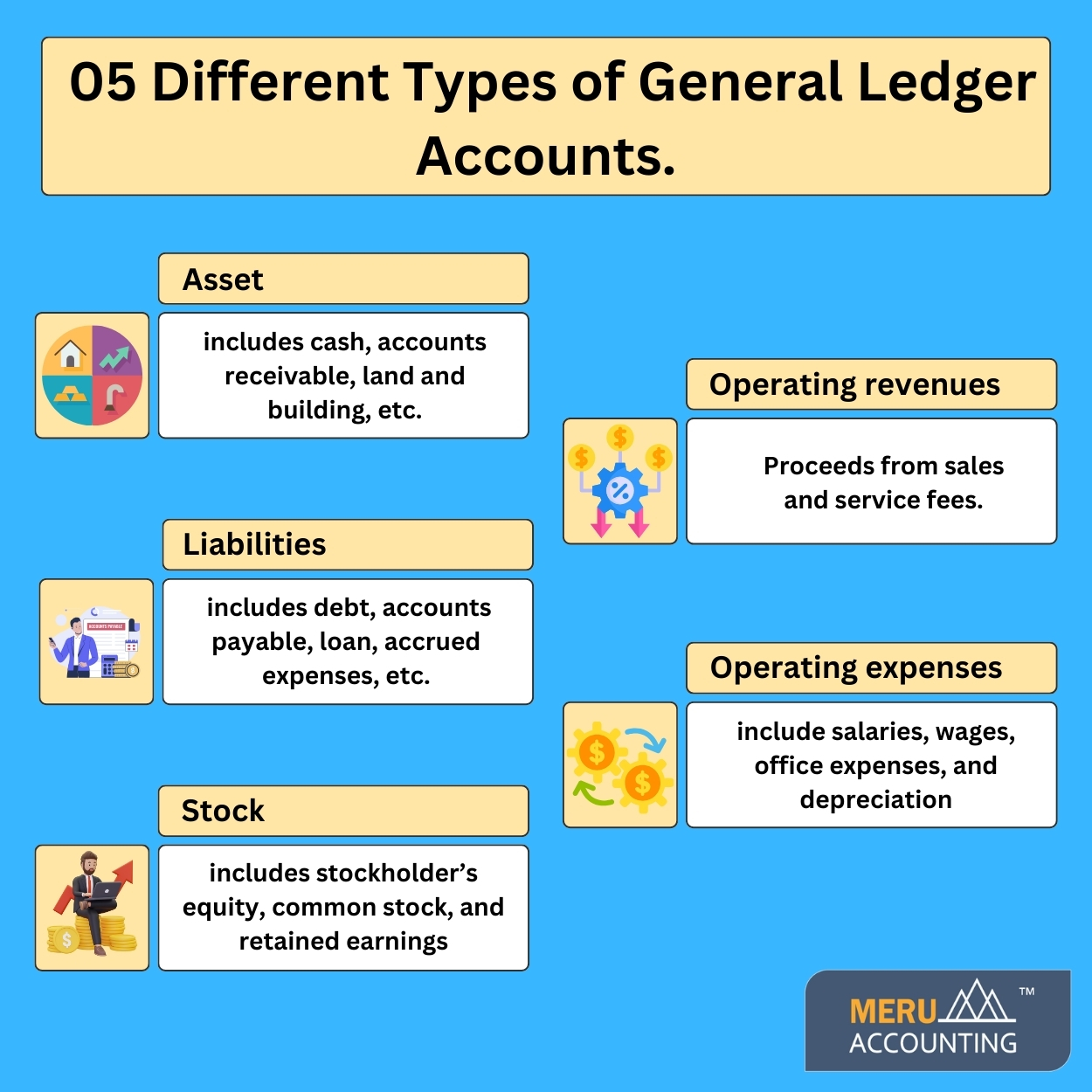

1. Asset:

It includes cash, accounts receivable, land and building, etc.

2. Liabilities:

It includes debt, accounts payable, loan, accrued expenses, etc.

3. Stock:

It includes stockholder’s equity, common stock, and retained earnings.

4. Operating revenues:

Proceeds from sales and service fees.

5. Operating expenses:

It include salaries, wages, office expenses, and depreciation.

Apart from these five general ledger account types, there also non-operating revenue and gains and non-operating expenses and losses accounts.

The information from the asset, liabilities, and stock flows into the balance sheet &

The information from operating and non-operating revenue and expenses flows into the income statement.

How does it work? Ledger accounts with example.

The financial transaction of the business is recorded as journal entries and then posted to the respective ledger accounts. Let’s understand the ledger posting with an example:

For example

Mr. David Dhawan has started a forging factory. On 1st January he started the business for $100,000. He opened a current account and deposited $400,000. The following are the transactions related to his factory.

| Particular | Amounts |

| Purchases (including credit purchases of $200,000) | $600,000 |

| Sale (credit sales of $50,000) | $800,000 |

| Rent | $150,000 |

| Wages | $15,000 |

| Depreciation on machinery @10 pa | $5,000 |

| Interest expenses | $25,500 |

| Principal returned to bank | $50,000 |

| Cash Account | |||||||

| Date | Particulars | Jr | Amount | Date | Particulars | Jr | Amount |

| 1/1/23 | To capital a/c | $100,000 | 1/1/23 | By Wages | $15,000 | ||

| To sales a/c | $400,000 | By bank a/c | $400,000 | ||||

| By balance c/d | $85,000 | ||||||

| $500,000 | $500,000 | ||||||

| Bank Account | |||||||

| Date | Particulars | Jr | Amount | Date | Particulars | Jr | Amount= |

| 1/1/23 | To cash a/c | $400,000 | 1/1/23 | By rent a/c | $15,000 | ||

| By interest exp | $25,000 | ||||||

| By bank loan | $50,000 | ||||||

| By balance c/d | $310,000 | ||||||

| Wages Account | |||||||

| Date | Particulars | Jr | Amount | Date | Particulars | Jr | Amount |

| 31/1/23 | To cash a/c | $15,000 | 31/1/23 | By balance c/d | $15,000 | ||

| $15,000 | $15,000 | ||||||

| Depreciation Account | |||||||

| Date | Particulars | Jr | Amount | Date | Particulars | Jr | Amount |

| 31/1/23 | To Machinery a/c | $5,000 | 31/1/23 | By balance c/d | $5,000 | ||

| 15,000 | $5,000 | ||||||

Above is an example of a ledger account. The ledger account includes the date, journal folio, particulars, and amount details of the financial transaction.

The preparation of the journal and ledger is based on the double-entry bookkeeping system. This system records every transaction when the money leaves the account (credit) and again when the money enters the account (debit). It works on the golden principles of accounting.

Don’t want to mess up with making ledger postings, hire an outsource bookkeeping service like us. Meru Accounting provides bookkeeping and accounting service at affordable rates.

Schedule a no-obligation appointment with us now.